Op-Ed: Why our health care costs are so high — and keep rising

Read original post on NJ Spotlight News, May 21, 2024

Why are health care costs rising so fast?

I put that question to my Rutgers University graduate students in the first session of their health policy course each year. Most of them have or will go on to leadership roles in government or the private sector, so it is important that they grasp issues as important as this one. The U.S. spends about twice as much per capita on health care as the average of other developed countries, and we don’t have better outcomes to show for our outsized spending.

Top answers that my students give to this question — before doing the assigned reading — include population growth, an aging society and poor health habits leading to more chronic illness. Nope, none of these responses come close to explaining why health care spending consistently rises faster than the U.S. economy as a whole. While it is true that the population is growing and aging, those trends are much slower than the health care spending trend. The prevalence of some chronic illnesses is also rising, but long-term trends like the decline in tobacco consumption have driven disease rates in the other direction.

So, what is the big health care spending driver? The late Princeton University professor and renowned health policy scholar Uwe Reinhardt put it succinctly: “It’s the prices, stupid.”

Measuring prices for health care services is challenging, not just for research but, more importantly, for consumers. In fact, health care may be the only service where we consumers typically don’t know its price until after we have purchased the product. Still, economists are able to disentangle trends, constantly showing that prices are by far the biggest long-term driver of rising spending.

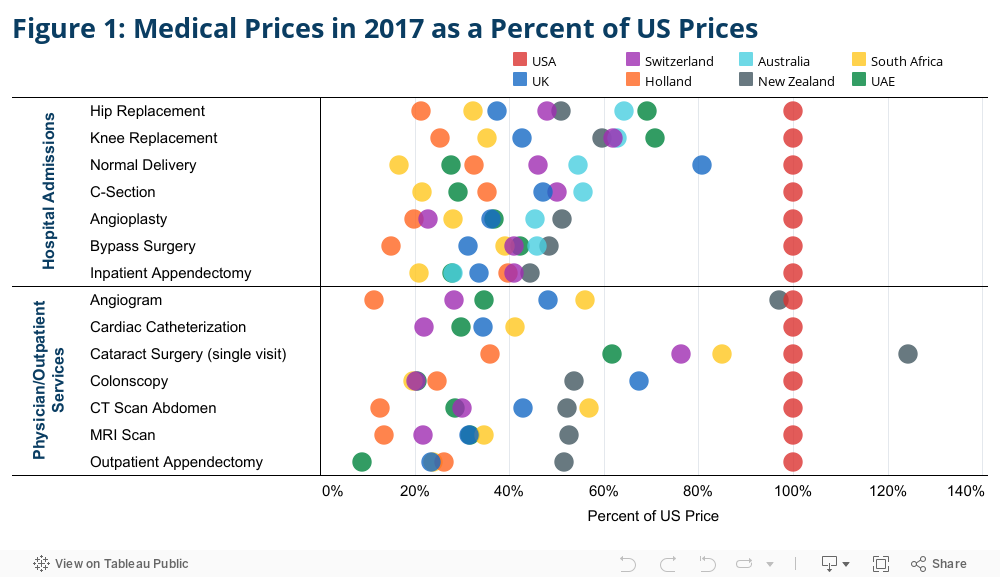

The U.S. stands alone in the way health care prices are determined, relying largely on private negotiations between health systems and insurance companies. The implications of this feature of our system are illustrated clearly in international comparisons. The linked chart, seen below, compares prices for selected hospital and ambulatory services as a precent of the average amount paid in the U.S. (You can view more detailed comparisons at this interactive report from the nonprofit Health Care Cost Institute.)

Consolidation a big factor

A large body of research by economists demonstrates that consolidation of hospital systems is a leading driver of prices. Studies clearly show that hospital mergers and acquisitions lead not only to higher hospital charges to insurance companies and patients, but also to diminished quality of care and customer service. One study published last year shows that accumulation of hospital market power also appears to drive down wages for nurses, even as many argue that there are shortages of these essential members of the health care team.

View Tableau Interactive Chart: Medical Prices in 2017 as a Percent of US Prices

There are other drivers of higher prices, especially for patent-protected pharmaceuticals, but hospital services represent nearly a third of all national health spending, while retail pharmacy accounts for only 9% of spending. Hospital market consolidation is set to drive costs still higher, even if the pace of such transactions slows. About 80% of hospital markets are considered “highly concentrated,” regulatory speak for monopolistic, by the U.S. Department of Justice and Federal Trade Commission. Moreover, exacerbating the effects of hospitals merging with other hospitals is the accelerating trend of hospital systems acquiring physician practices. Combined hospital and physician and related services represents half of all health care spending in the U.S.

NJ not unique

Using New Jersey hospital cost reports — obtained under our state’s embattled Open Public Records Act — my co-authors and I conducted a study that strongly suggests that New Jersey can expect rising hospital prices for years to come. By 2020, the last year of our study, 71% of hospital admissions were in highly concentrated markets, using standards established by the Department of Justice and the FTC. New Jersey hospital mergers and acquisitions proceeded at a steady pace in most of the 11 years of our study, despite recent federal interventions to block some transactions in the state.

Our analyses reveal a close association between the market consolidation trend and rising hospital profitability, no doubt driven by price increases. Even if regulators are vigilant and prevent further consolidation, New Jersey’s already consolidated hospital systems are positioned to demand high prices from insurers and consumers. Casual observation of branding on doctors’ offices suggests that hospital system acquisition of community practices is the next frontier of consolidation, as has been documented nationally. These trends raise serious concerns for future health care affordability for New Jersey consumers.

What to do

The federal government is front and center in antitrust enforcement, but federal law and jurisprudence leave yawning gaps for stemming anticompetitive behavior in health care markets. In fact, federal policy is making a bad problem worse, as Medicare pays more to hospital-owned physician practices for the same services than to non-hospital owned practices. Further, federal agencies responsible for addressing the problem are hamstrung by inadequate budgets and legal constraints, like gaps in jurisdiction over mergers by not-for-profit organizations. (Most hospital systems in New Jersey are nonprofits.)

With or without needed federal policy reforms, states must step up. State government is well positioned and has the authority to address the harms of anticompetitive behaviors while promoting excellence in health care delivery. State policy leaders know their populations’ health needs and care delivery systems better than distant federal agencies.

What can states do? Most importantly, they should closely monitor and exercise approval authority over consolidation by health care providers. Federal agencies monitor only large transactions, so states should review and provide oversight to smaller proposed acquisitions and mergers. Over time, small transactions can lead to the accumulation of excessive market power. Review should be pre-transactional, before the providers expend resources to execute mergers, and monitoring should continue after approved mergers and acquisitions are implemented.

States should also require routine reporting and routinely monitor trends in ownership of medical practices — not just by hospital systems, but private equity firms and other financial players that are increasingly poised to drive cost and diminish quality. Proactive measures can help pre-empt problems rather than waiting for fallout from mergers and acquisitions on prices and quality.

States vary in their approaches to promoting competition in health care delivery, and New Jersey’s approach is stronger than most. Still, New Jersey should expand the scope of transactions subject to review. Such actions would build on other recent New Jersey initiatives addressing health care affordability, including the Health Care Affordability, Responsibility, and Transparency (HART) Program and the recently enacted Prescription Drug Affordability Council. (In full disclosure, my team at the Center for State Health Policy are advisers to the HART Program.)

These are critically important actions, but our state should not wait to robustly address provider prices, a well documented force increasing health care costs to which New Jersey is not immune.

Joel C. Cantor, ScD, is a Distinguished Professor of Public Policy and founding Director of the Center for State Health Policy